P2P Financing in Malaysia: A Complete Guide for SMEs (2026)

This guide explains how P2P financing works, what the regulations require, and where the real risks lie for SME borrowers. It also compares P2P with other financing options so you can choose the path that suits your business.

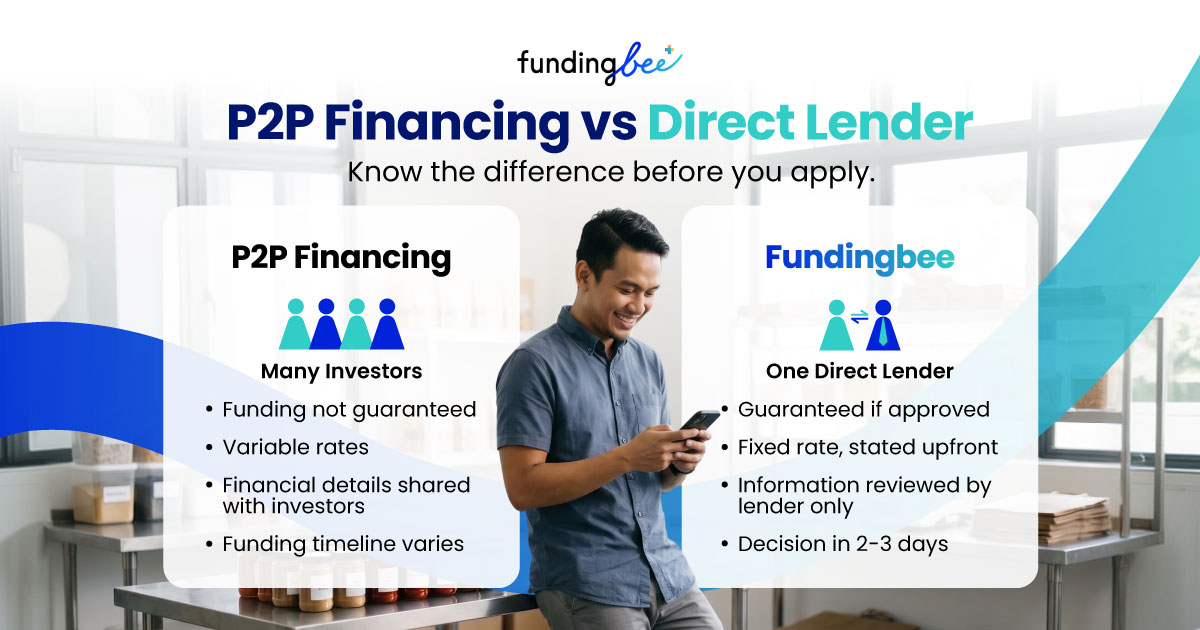

P2P financing is one of the fastest-growing alternatives to bank loans in Malaysia. Before you apply, know one key point. Unlike a bank loan or a direct lender, P2P financing depends on investor demand. The platform can approve your application and list it publicly, but you might still fail to raise the full amount you need.

What Is P2P Financing in Malaysia?

How Peer-to-Peer Financing Works

P2P financing connects businesses that need capital directly with investors through a licensed online platform. The platform does not lend its own money.

It acts as a marketplace: it lists your funding request publicly, and investors choose whether to fund it.

A typical P2P financing cycle works as follows:

- You submit your business financials and a funding request to the platform.

- The platform assigns a risk grade and lists your campaign to investors.

- Investors review your financials and decide whether to participate.

- Once the minimum funding target is reached, the funds are released to you.

- You repay in instalments over an agreed period, typically 3 to 12 months.

One important detail: your financial information, risk grade, and business profile are visible to all investors on the platform. This is different from applying to a bank or a private lender, where your information stays confidential.

Who Regulates P2P Financing in Malaysia?

The Securities Commission Malaysia (SC) registered the first six P2P operators in 2016 [1], making Malaysia the first ASEAN country to regulate P2P financing. Platforms must register as Recognised Market Operators (RMOs) under the Guidelines on Recognised Markets [2], with requirements including a minimum paid-up capital of RM5 million and segregated trust accounts. A full list of registered operators is available on the SC Digital Initiatives page [3]. Since the framework launched, P2P financing has cumulatively raised RM7.9 billion in Malaysia as of September 2024 [4].

P2P Financing vs Other SME Financing Options in Malaysia

P2P Lending vs Bank Loans vs Direct Licensed Lenders

No single financing option suits every business. The three most common routes for Malaysian SMEs are conventional bank loans, P2P financing, and direct licensed lenders. Each has a different risk profile, approval timeline, and ideal use case.

When Each Option Makes Sense

- Bank loan: best for established businesses needing large amounts (RM100,000 and above) with collateral and at least 3 years of audited accounts.

- P2P financing: suitable for SMEs needing RM50,000 and above, comfortable with public financial disclosure, and willing to wait 2 to 4 weeks for investor funding.

- Direct licensed lender (e.g. FundingBee): best for SMEs needing RM5,000 to RM50,000 with a 2-year or more operating history who require fast, certain, and private funding.

The Pros and Cons of P2P Lending in Malaysia

Potential Benefits of P2P Financing for SMEs

- No collateral required in most cases, unlike conventional bank loans.

- Accessible to SMEs that do not meet strict bank requirements, including businesses with limited credit history.

- Higher loan ceilings than most micro-lenders. The SC permits issuers to raise up to RM10 million per campaign

- Shariah-compliant options are available on certain platforms, such as microLEAP

- Government support: the SC's SARANA scheme (launched January 2025) channels P2P financing to SMEs on government procurement contracts

Risks and Drawbacks SME Borrowers Should Know

The following risks are specific to P2P financing from a borrower's perspective and are often underweighted when businesses compare options.

- Funding is not guaranteed. Your campaign can be approved, listed, and still not reach its target if investor demand is insufficient. You may wait weeks and receive nothing.

- Your financials are public. The platform shares your financials, risk grade, and business profile with all registered investors — a level of disclosure not required by banks or private lenders

- Interest rates vary. Your effective borrowing cost depends on your risk grade and the competitive environment among other issuers. Rates are not always predictable in advance.

- Platform fees add to the total cost. Beyond interest, P2P platforms typically charge a service fee that varies by loan size and risk grade.

- Repayment timelines are short. Most P2P facilities run for 3 to 12 months, which can create cash-flow pressure for businesses with longer revenue cycles.

- Credit history affects your terms. Applicants who turn to P2P often have weaker credit profiles, which can result in higher risk grades and higher effective rates.

A Safer Alternative: Direct Licensed SME Financing with FundingBee

Why FundingBee Is a Lower-Risk Choice for SMEs

FundingBee by Bee Informatica Sdn Bhd is not a P2P platform. It is a direct money lender licensed by KPKT (Kementerian Perumahan dan Kerajaan Tempatan), Licence No. WL7517/14/01-3/051026 [5].

This distinction matters for SME owners in three specific ways:

- Funding certainty. When your application is approved, the funds are committed. No crowdfunding campaign, no investor pool to fill, no risk of partial funding.

- Private financial disclosure. Your business information is shared only with FundingBee, not published to a pool of investors.

- Transparent, fixed terms. 16% annual interest plus an 8% one-time processing fee. No hidden charges or variable rates tied to investor sentiment.

FundingBee Loan Features at a Glance

Try the FundingBee Loan Calculator

Want to see your estimated repayment before applying? Use the business loan calculator to run the numbers in under 30 seconds.

Conclusion: Choosing the Right Financing Path for Your SME

P2P financing is a legitimate, well-regulated option backed by the Securities Commission Malaysia, with over RM7.9 billion raised since 2016 [4]. However, it is not the right fit for every situation. If your business needs speed, confidentiality, and an amount between RM5,000 and RM50,000, the uncertainty of crowdsourced investor demand can be a genuine obstacle.

The right question is not which option sounds best on paper.

Which option gives you the certainty, speed, and terms your business needs right now.

Frequently Asked Questions (FAQ)

These FAQs address the questions most commonly searched by Malaysian SME owners exploring financing options.

Is P2P financing legal in Malaysia?

Yes. P2P financing is fully regulated under the Securities Commission Malaysia. All platforms must register as Recognised Market Operators (RMOs) [2]. Malaysia was the first country in ASEAN to regulate P2P financing, introducing the framework in 2016 [1]. Only use platforms that appear on the SC's official registered operator list [3].

What is the difference between P2P financing and a bank loan?

A bank loan comes from a single institution with fixed terms and a private approval process. P2P financing raises money from a pool of investors via a public online campaign. Your financial information is visible to investors, and your funding is not guaranteed until the campaign is fully subscribed. Banks also typically require collateral and longer operating histories, while P2P platforms may be more accessible to newer SMEs.

How much can I borrow through P2P financing in Malaysia?

The Securities Commission Malaysia allows issuers to raise up to RM10 million through P2P platforms [2]. For smaller amounts, typically RM5,000 to RM50,000, a direct licensed lender such as FundingBee may offer faster and more certain access to funds without the need for a public funding campaign [5].

Is P2P financing Shariah-compliant?

Some P2P platforms in Malaysia offer Shariah-compliant structures alongside conventional options [6]. Platforms such as microLEAP operate both streams. Shariah-compliant campaigns accounted for approximately 15% of total P2P funds raised in Malaysia as of the end of 2023. If Shariah compliance is a requirement, confirm the structure directly with your chosen platform before applying.

References

All factual claims in this article are drawn from the following authoritative sources.

1. Securities Commission Malaysia. SC Announces Six P2P Financing Operators (Malaysia first in ASEAN)

2. Securities Commission Malaysia. Guidelines on Recognised Markets (ECF, P2P)

3. Securities Commission Malaysia. Digital Initiatives: Registered P2P Operators

4. TechNode Global / SC. SC Launches SARANA; P2P financing reaches RM7.9 billion (January 2025)

5. FundingBee by Bee Informatica Sdn Bhd. KPKT Licence No. WL7517 | fundingbee.my

6. FintechNews Malaysia. A List of Licensed P2P Platforms in Malaysia