Capital Loan Malaysia: 5 Smart Ways to Fund Your Business Growth Without Draining Your Savings

The fastest-growing Malaysian SMEs rarely fund expansion from savings alone. They combine government grants, smart borrowing, and the right type of capital loan for the right purpose. That mix, not the size of the loan, protects cash flow as a business scales.

Malaysia's small and medium enterprises now contribute 39.5% of the national GDP and make up 96.1% of all business establishments [1]. Growth at this scale needs capital, but capital does not have to mean draining a business's cash reserves. This guide breaks down five practical ways Malaysian business owners fund growth in 2026, what lenders actually check before approving a capital loan, and the most common mistakes to avoid along the way.

Capital Loan vs Working Capital Loan: What Is the Difference?

A capital loan funds growth. A working capital loan funds operations. Mixing the two up is one of the most common and most costly planning mistakes Malaysian SME owners make.

A capital loan is often used for one-time or growth-stage investments. Examples include a second outlet, a new production line, a delivery fleet, or a major equipment upgrade.

A working capital loan, on the other hand, covers the everyday cash flow gaps between paying suppliers and collecting from customers, things like stock purchases, payroll, and rent.

Startup Capital vs Growth Capital vs Cash Flow Capital

Business owners usually need different types of capital at different stages:

- Startup capital — funds the initial setup: renovation, licensing, first batch of stock or equipment.

- Growth capital — funds for expansion once the business is already generating revenue: a second branch, new machinery, additional staff.

- Cash flow capital — short-term funding that smooths out timing gaps, such as waiting 30 to 60 days for B2B customers to pay invoices.

Borrowing short-term for a long-term asset, or the reverse, is a quiet way businesses overpay on financing.

Choosing the Right Loan Horizon: Short-Term vs Long-Term

A good rule of thumb: match the loan tenure to the lifespan of what it is funding.

- Buying a vehicle or machinery that will be used for 5 years → a longer-tenor loan spreads the cost more sensibly.

- Bridging a 60-day gap before a large invoice is paid → a short-term facility avoids paying years of interest on a temporary need.

Borrowing short-term for a long-term asset (or the reverse) is one of the quiet ways businesses end up overpaying on financing.

5 Smart Capital Funding Strategies for Malaysian Business Owners

Most growing SMEs in Malaysia do not rely on a single source of financing. They layer a few of the following strategies based on what they are funding and how fast they need it.

1. Use Term Loans for Asset Purchase (Equipment, Machinery, Vehicles)

A term loan, a lump sum repaid over a fixed schedule, is generally the most cost-efficient way to fund a one-time asset purchase. For example, a workshop owner upgrading to a new alignment machine, or a manufacturing SME adding a second production line, benefits from spreading the cost over the asset's useful life rather than paying for it upfront.

Banks typically require the asset itself as partial security, which can lower the interest rate compared to an unsecured facility. The trade-off is a longer approval process and more extensive documentation.

2. Tap Government Grants & Low-Cost Financing Before a Commercial Loan (Budget 2026 Highlights)

You do not need to repay grants, so you should look for them first before you apply for a loan. Budget 2026 expanded several SME-focused programmes that growth-minded business owners can combine with financing:

- MSME Digital Grant Madani — a 50% matching grant of up to RM5,000 for SMEs adopting approved digital tools, administered through BSN and MDEC-listed technology providers [2].

- BNM Automation and Digitalisation Facility (ADF) — a low-interest financing facility from Bank Negara Malaysia, open to all Malaysian SMEs, that supports the purchase of equipment, machinery, and IT systems at a financing rate of up to 4% per annum, with financing of up to RM3 million per SME and tenure of up to 10 years [3]. Unlike a grant, this is financing that is repaid — but at a meaningfully lower cost than typical commercial rates.

- SJPP Government Guarantee Scheme MADANI — the government guarantees a large portion of a bank loan, which can reach up to 80% coverage for eligible SMEs, making banks more willing to approve financing for businesses with limited collateral or track record [4].

These programmes can meaningfully lower the total cost of a growth project. A capital loan can then fill the remaining gap that grants and guarantees do not cover.

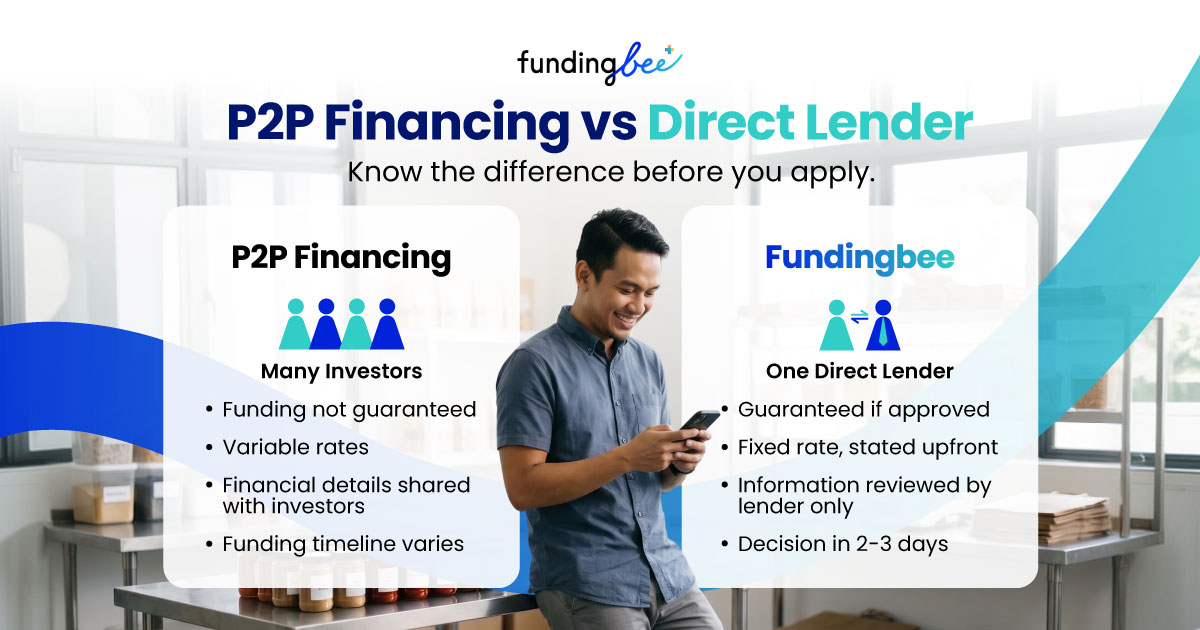

3. Use P2P Financing for Expansion Capital Without Giving Up Equity

Peer-to-peer (P2P) financing lets a business borrow from many investors through an online platform. The platform is regulated by the Securities Commission Malaysia (SC).

This avoids giving up equity or waiting for long bank approvals [5]. Malaysia was the first ASEAN country to introduce a formal regulatory framework for P2P financing in 2016 [6].

The sector has grown quickly: as of end-2023, around RM5.96 billion had been raised through P2P platforms in Malaysia since launch [6]. Notably, wholesale and retail trade was the single largest sector funded through P2P platforms in 2023, raising over RM1.12 billion [6] — a sign of how mainstream this option has become for everyday Malaysian retailers and traders looking to restock or expand without diluting ownership.

4. Go Non-Bank for Speed & Flexibility — Best for Growing SMEs

Traditional banks remain a strong option for SMEs with a long track record, full financial statements, and collateral. For businesses that do not fit that profile, licensed non-bank lenders fill a real gap. This includes newer F&B outlets, sole proprietors without audited accounts, and owners who need decisions in days.

A KPKT-licensed non-bank lender typically asks for fewer documents, assesses eligibility faster, and is often more flexible on collateral requirements. Non-bank financing often has a lower loan limit and a shorter term than a bank loan. It works well to bridge or top up a growth project, not to fund it fully.

5. Stack Micro + Business Loans to Bridge Capital Gaps Strategically

It is now common, and not discouraged, for Malaysian SME owners to have financing from more than one lender. Each lender can serve a different purpose. A micro loan might cover a quick stock top-up, while a separate business loan funds a renovation or new equipment.

The key is to review each lender's eligibility rules up front. Do not assume a past loan blocks a new application. Many Malaysian SME owners use financing from more than one platform or institution at once. This works well if each facility pays on time.

Capital Loan Eligibility in Malaysia — What Lenders Actually Check

Eligibility criteria vary between banks and non-bank lenders, but most assessments come down to three things.

SSM Registration & Minimum Business Operating Period

Almost every lender requires the business to be registered with the Companies Commission of Malaysia (SSM) and to have a minimum operating history. Six months of operations is a common minimum threshold across SME grant and financing programmes in 2026 [7]. Individual lenders may set different requirements.

Minimum Annual Turnover Requirements

Lenders generally want to see consistent revenue, not necessarily a large one. A clear pattern of monthly sales, even if modest, often matter more to an underwriter than a single strong month followed by a quiet one.

CTOS / CCRIS Health Check

Before approving any facility, lenders check a business and its directors against Malaysia's two main credit reference systems: CCRIS, the Central Credit Reference System managed by Bank Negara Malaysia, and CTOS, a licensed private credit reporting agency that issues the MyCTOS Score Report [8]. A clean repayment history on existing facilities, even small ones, strengthens a new application far more than having no credit history at all.

Fumiko, CEO of FundingBee, also discusses her own experiences in this article.

SME Loan Approval Secrets: What Lenders Look for in RM5k–RM50k Applications

Capital Loan Pitfalls Every Malaysian SME Owner Must Avoid

Over-Borrowing Beyond Your Repayment Capacity

A larger approved amount is not always the better choice. Borrowing close to the maximum a lender offers, rather than the amount the growth project actually needs, is one of the most common ways in which healthy SMEs end up overleveraged within a year or two.

Using Capital Loans to Cover Day-to-Day Operating Expenses

A capital loan is structured around a growth project with a clear return, such as new equipment or a second outlet. Using it instead to cover recurring shortfalls, rent, payroll, or supplier payments, usually signals a cash flow problem. A term loan will not fix this. You may need a working capital facility instead. You may also need to review the business's pricing and costs.

How FundingBee Helps Malaysian Businesses Access Growth Capital Fast

For SME owners who have already explored grants and bank options but still need fast, flexible funding to act on a growth opportunity, FundingBee can help. FundingBee is a KPKT-licensed (Licence No. WL7517) non-bank lender built specifically for Malaysian SMEs that banks often overlook.

Loan Amounts, Tenure & Flexible Repayment Options

FundingBee offers business loans from RM5,000 to RM50,000. These loans fit the growth plans most Malaysian SMEs are making. Use them for restocking before a busy season. You can also fund a small equipment upgrade. You can top up your renovation budget too. Repayment terms match your business cash flow. They do not use a one-size-fits-all schedule.

No Collateral Required

Because approval is based on the business's operating history and repayment capacity rather than fixed assets, FundingBee does not require collateral, which matters most for F&B outlets, retailers, and service businesses that may not hold the kind of property or heavy machinery that banks typically require as collateral for a loan.

If a growth opportunity fits this profile, check eligibility soon on FundingBee. It should be fast-moving, collateral-light, and time-sensitive.

Conclusion: Fuel Your Growth with the Right Capital Loan

Growth capital is not about choosing the largest available loan; it is about matching the right funding source to the right purpose at the right time. Government grants reduce upfront cost.

Term loans fund long-life assets. P2P financing and non-bank lenders fill the gaps that banks move too slowly to cover. Used together and carefully checked against eligibility requirements rather than assumptions, these tools allow a Malaysian SME to grow without putting its savings or stability at risk.

Ready to see what you qualify for? Register an account and apply for a FundingBee Micro Business Loan to find out how fast your growth plan could be funded.

References

[1] Department of Statistics Malaysia (DOSM) — Small and Medium Enterprises (SMEs) Performance 2024. https://www.dosm.gov.my/portal-main/release-content/micro-small--medium-enterprises-msmes-performance-2024

[2] Bank Simpanan Nasional (BSN) — MSME Digital Grant MADANI. https://www.bsn.com.my/page/MSMEMadani

[3] Bank Negara Malaysia — Additional Allocation of RM700 Million for the SME Automation and Digitalisation Facility. https://www.bnm.gov.my/-/additional-allocation-rm700-million-sme-adf

[4] Syarikat Jaminan Pembiayaan Perniagaan Berhad (SJPP) — Government Guarantee Scheme MADANI. https://www.sjpp.com.my/

[5] Securities Commission Malaysia — Frequently Asked Questions on the Peer-to-Peer Financing (P2P) Framework. https://www.sc.com.my/regulation/regulatory-faqs/frequently-asked-questions-on-the-peer-to-peer-financing-p2p-framework

[6] Capital Markets Malaysia — Peer-to-Peer (P2P) Financing. https://www.capitalmarketsmalaysia.com/digital-peer-to-peer-p2p-financing/

[7] Press (Digital PR Malaysia) — How to Apply for 2026 SME Grants & Digitalisation Funds. https://www.press.com.my/accounting-tax/how-2026-sme-digitalisation-grants/

[8] UOB Business Insights — Get Your SME Loan Approved with the Help of the SJPP Loan Scheme. https://www.uob.com.my/business/sme-hub/insights/get-your-sme-loan-approved.page

.png)