SME Loan Malaysia 2026: 7 Best Financing Options You Haven't Tried Yet

This guide outlines seven SME funding options in Malaysia for 2026. It explains each option’s benefits, ideal applicants, and how to decide.

Why most Malaysian SMEs Still Struggle to Get Funded

Malaysia has over 1.08 million MSME establishments, accounting for 96.1% of all businesses, 39.5% of GDP, and 48.7% of national employment.*1

Despite this scale, access to formal financing remains a persistent gap. This is especially true for micro and early-stage businesses. They often do not meet commercial bank eligibility requirements. BNM's Financial Inclusion Framework 2023–2026 explicitly identifies improving MSME access to financing as a national priority.*²

The good news? More options exist in 2026 than ever before. From government-backed schemes to fast-approval non-bank lenders, this guide covers 7 financing options worth considering — ranked by accessibility.

What Counts as an SME in Malaysia? (SSM & SME Corp Definition 2026)

Micro, Small & Medium — Where Does Your Business Fit?

Under SME Corp Malaysia's definition*3, SMEs are categorised by annual sales turnover and number of full-time employees. Micro businesses earn under RM300,000 annually; small businesses up to RM15 million; medium businesses up to RM50 million.

Why Your SME Classification Directly Affects Your Loan Options

Different lenders serve different tiers. Banks often want strong financial statements from mid-sized firms. Micro and small businesses may have better options. They can look into government microloans or alternative lenders.

7 SME Financing Options in Malaysia (Ranked by Accessibility)

1. Bank Negara Malaysia (BNM) Special Fund Schemes

BNM offers subsidised financing through schemes such as the Automation and Digitalisation Facility (ADF), with financing rates of up to 3.75% per annum inclusive of a guarantee fee, and a maximum loan amount of RM5 million per SME.*4 All applications are submitted through Participating Financial Institutions (PFIs) and are subject to the PFI's standard credit assessment process.

2. SME Corp Malaysia Financing Programmes

SME Corp administers grants and soft loans targeting innovation, export readiness, and productivity. These are suited to SMEs with documented growth plans and complete financial records.

3. Commercial Bank SME Loans (Maybank, CIMB, RHB)

Malaysia's major banks offer a wide range of SME loan products. Standard eligibility requirements include a minimum of 2 years of business operation, a clean CCRIS/CTOS credit record, and audited financial statements.

4. Development Financial Institutions — MIDF, BSN, PUNB

DFIs serve specific segments: MIDF for manufacturing and services, BSN for micro enterprises, and PUNB for Bumiputera entrepreneurs. Each institution sets its own financing rates in accordance with its mandate and target segment.

5. Government Micro Loans — TEKUN Nasional & MARA

TEKUN Nasional offers loans of up to RM100,000 at a flat rate of 4% per annum, with repayment periods of up to 10 years.*5 Audited financial statements are not required. MARA operates separate schemes with its own eligibility criteria, primarily targeting Bumiputera applicants.

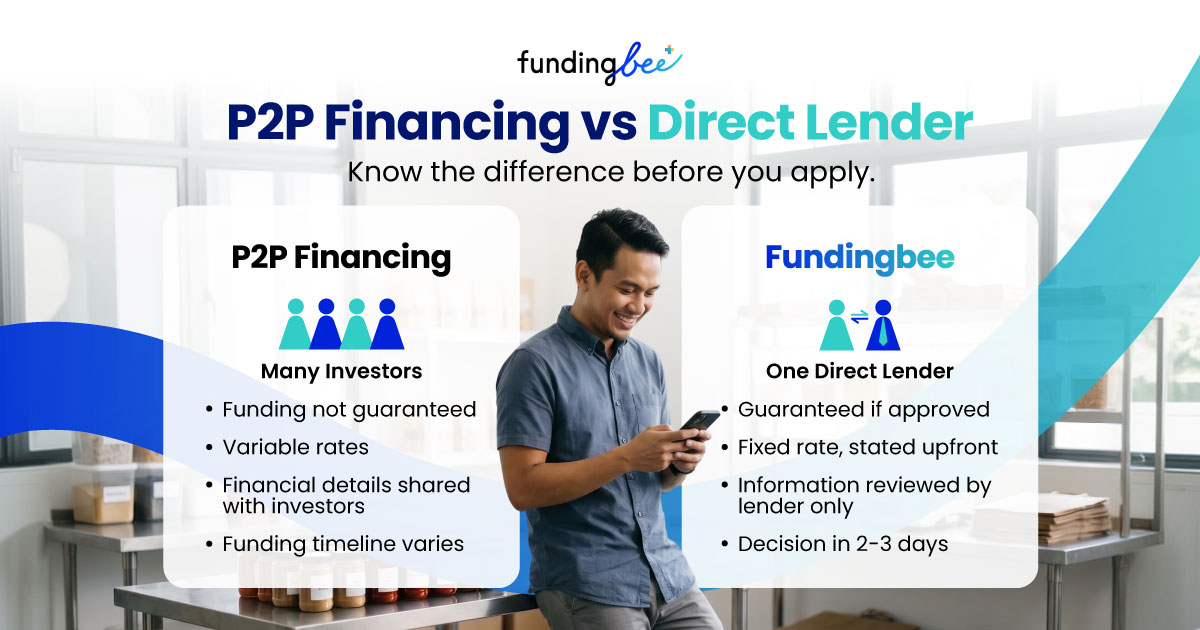

6. SC-Licensed P2P Financing Platforms

The Securities Commission Malaysia (SC) licenses P2P platforms as Recognised Market Operators and caps financing rates at 18% per annum under its Guidelines on Recognised Markets.*6 Rates vary by platform and borrower risk profile. SC-licensed P2P platforms operate on an unsecured basis — no physical collateral is required from the issuer.

7. Non-Bank Lenders — Like FundingBee

Licensed non-bank lenders such as FundingBee (KPKT-licensed) offer a practical alternative for SMEs that do not meet bank criteria. With minimal documentation, flexible loan amounts from RM5,000, and approvals often within days, non-bank financing is increasingly popular among micro and small businesses.

How to Choose the Right SME Loan for Your Situation

By Business Type

Retail and F&B businesses benefit from flexible repayment structures that align with cash flow cycles. Service-based businesses may qualify for invoice financing, while manufacturers can tap DFI-specific programmes.

By Loan Amount (RM10K–RM500K)

For amounts under RM50,000, microloan programmes and non-bank lenders are usually the most accessible options. Commercial banks and DFIs suit RM50,000–RM500,000 if you meet the documentation requirements.

By Urgency — How Fast Do You Need the Funds?

Government schemes route applications through PFIs and involve standard credit assessments, which require additional processing time. Non-bank lenders and some P2P platforms process applications and disburse funds within days.

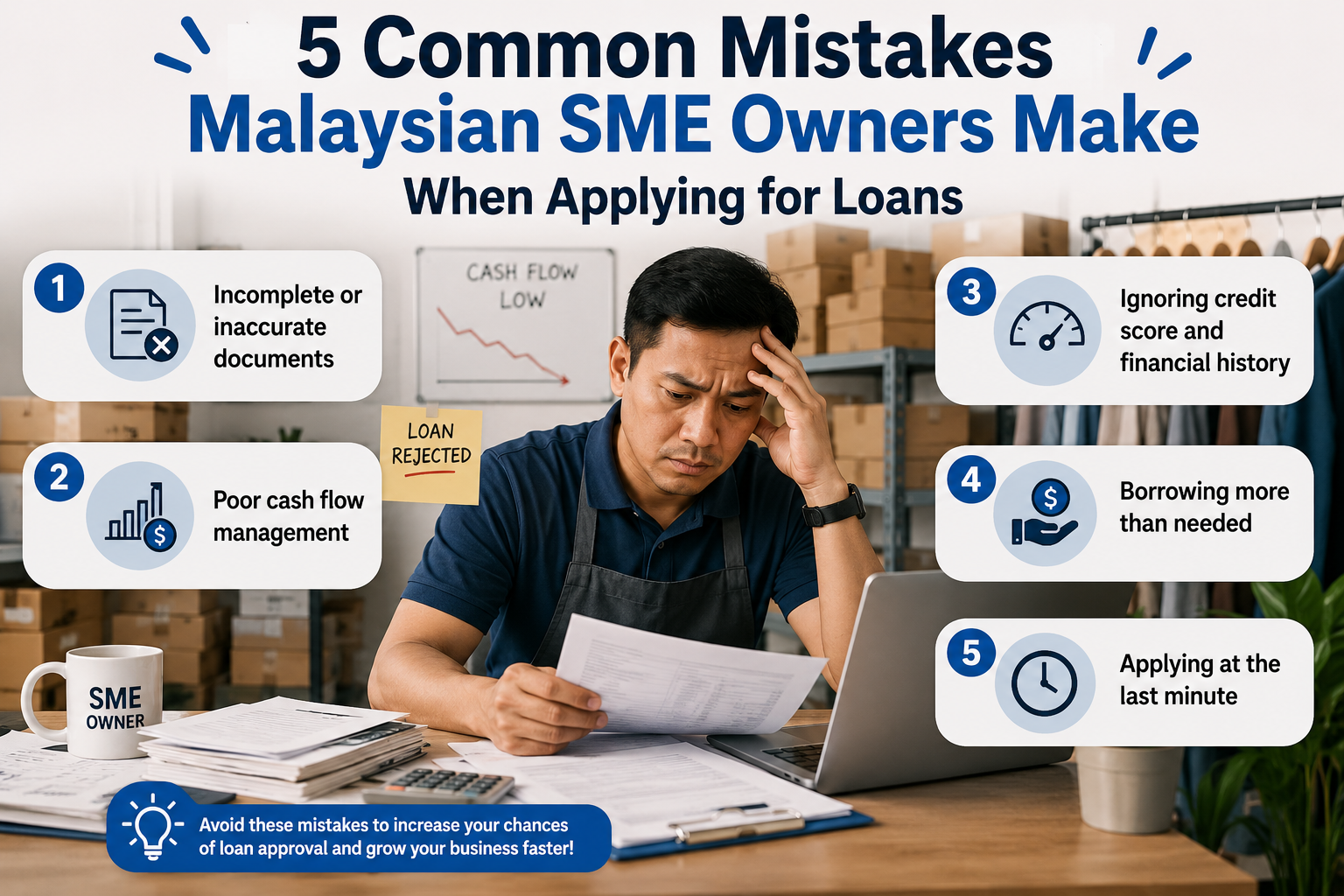

5 Common Mistakes Malaysian SME Owners Make When Applying for Loans

1. Applying to the Wrong Lender for Your Business Profile

Many SME owners apply to banks first — only to be rejected due to insufficient operating history or documentation. Understanding each lender's eligibility criteria before applying saves time and avoids unnecessary credit record enquiries.

2. Submitting Incomplete or Outdated Documents

Most rejections come down to incomplete paperwork. Always prepare updated bank statements (last 3–6 months), a valid SSM registration, and your latest tax returns before submitting any application.

3. Not Maintaining Sufficient Cash Balance Before Applying

Lenders use your bank statements to assess repayment capacity. According to FundingBee CEO Fumiko, the benchmark is a cash balance of approximately three times your expected monthly repayment.*7 Consistently ending the month with a minimal balance is one of the most common reasons for rejection.

4. Not Separating Personal and Business Finances

Using a personal bank account for business transactions makes it difficult for lenders to accurately assess your business cash flow. Maintaining a dedicated business account is a basic requirement for most loan applications and demonstrates financial discipline to lenders.

5. Applying Without Checking Eligibility Requirements First

Each lender has its own eligibility criteria, required documents, and loan terms. Submitting an application without first reviewing these often leads to back-and-forth requests for additional information, which take time for both the applicant and the lender to resolve. Before applying, confirm that your business meets the lender's basic requirements and that your documents are complete. This makes the process faster and more straightforward for everyone involved.

Why FundingBee Fills the Financing Gap for Malaysian SMEs

FundingBee is a KPKT-licensed non-bank financing provider designed for Malaysian SMEs and micro-businesses that do not meet the criteria of traditional banks. We offer loan amounts from RM5,000, a straightforward application process, and fast approvals — without the lengthy paperwork.

Whether you're a sole proprietor or a growing SME, FundingBee exists to help you access the capital you need — responsibly and transparently.

Conclusion

Finding the right SME loan in Malaysia takes more than just comparing interest rates. It's about matching your business profile to the right lender at the right time. Use this guide as your starting point. If banks have turned you down before, keep going. Alternative financing options like FundingBee are made for businesses like yours.

Frequently Asked Questions (FAQ)

Q1: What is the easiest SME loan to get approved for in Malaysia in 2026?

For businesses with few documents or a short history, non-bank lenders are often the easiest option. Government microloan programmes like TEKUN and MARA can also be easier to access. KPKT-licensed lenders like FundingBee also offer fast approvals with less paperwork. This makes them a strong option for micro and small businesses.

Q2: What documents do I need to apply for an SME loan in Malaysia?

Document requirements vary by lender. For most commercial bank SME loans, you will need: a valid SSM business registration, at least 6 months of business bank statements, your latest income tax return, and audited financial statements. Non-bank lenders typically require fewer documents — FundingBee, for example, accepts as few as 3 basic business documents.

Q3: How much can I borrow as a small business owner in Malaysia?

The amount you can borrow depends on which programme or lender you apply to. TEKUN Nasional offers up to RM100,000 in financing for micro-entrepreneurs.

BNM-funded schemes cap at RM5 million per SME while commercial banks offer up to RM10 million, depending on your financials. For smaller needs, non-bank lenders like FundingBee offer financing from RM5,000. This is a practical start for micro and early-stage businesses.

► Ready to grow your business? Apply for your SME loan with FundingBee today. Visit fundingbee.my to check your eligibility in minutes.

References

*1 Micro, Small & Medium Enterprises (MSMEs) Performance 2024: https://www.dosm.gov.my/portal-main/release-content/micro-small--medium-enterprises-msmes-performance-2024

*2 Bank Negara Malaysia — Financial Inclusion Framework 2023–2026:

https://www.bnm.gov.my/documents/20124/55792/SP-2nd-fin-incl-framework.pdf

*3 SME Definitions — SME Corp Malaysia https://smecorp.gov.my/index.php/en/policies/2020-02-11-08-01-24/sme-definition

*4 The SME Stabilisation Relief Facility (SME SRF) — Bank Negara Malaysia https://www.bnm.gov.my/funds4sme

*5 TEKUN Nasional — TEKUN Niaga Financing Scheme FAQ / TEMAN TEKUN FAQ (Official): https://www.tekun.gov.my/skim-pembiayaan-tekun-niaga-soalan-lazim/

*6 Capital Markets Malaysia (SC-endorsed) — Peer-to-Peer (P2P) Financing, citing SC Guidelines on Recognised Markets: https://www.capitalmarketsmalaysia.com/digital-peer-to-peer-p2p-financing/

*7 FundingBee — SME Loan Approval Secrets: What Lenders Look for in RM5k–RM50k Applications (19 February 2026): https://www.fundingbee.my/en/corporate-ceo/sme-loan-approval-secrets-what-lenders-look-for-in-rm5k-rm50k-applications

.png)